Agents for Risk Assessment and Fraud Detection in FinTech

Discover how agentic AI and Aegis enable real-time fraud detection, risk assessment, and compliance in FinTech without sacrificing user experience.

AI Agents for Risk Assessment and Fraud Detection in FinTech

The FinTech sector is under constant siege from evolving fraud tactics that exploit both scale and speed. As digital transaction volumes soar, legacy fraud detection systems—built on batch scoring and static rules—are increasingly unfit for the job. Deloitte projects that AI-enabled fraud losses could rise by over 60% by 2027, driven by generative AI and automated attack chains.

To combat this, forward-thinking security teams are exploring multi-agent AI architectures—coordinated networks of specialized agents that detect, assess, and mitigate fraud in real time. Yet, as enterprises embrace these systems, they face new operational risks: inter-agent coercion, over-privileged access, and opaque decision-making. This is where Aegis, the agentic security mesh by AegisSecurity provides the critical layer of trust, governance, and control.

The New Fraud Landscape in FinTech

From Rule-Based Defense to Adaptive Intelligence

Traditional fraud systems rely on hand-tuned rules and periodic model updates. While they’re easy to interpret, they fail against novel attack patterns such as synthetic identities, AI-generated documents, and automated account takeovers. These static systems create two core problems:

- High false positives, frustrating legitimate customers.

- Blind spots for novel attacks, especially across fragmented data streams.

In contrast, agentic fraud detection systems operate continuously. Agents collect telemetry from payments, KYC systems, devices, and external feeds, collaborating to assess risk dynamically. They adapt faster than rule sets ever could—if secured properly.

The Multi-Agent Fraud Pipeline

A modern FinTech fraud pipeline often involves:

- Signal Collector Agent – Aggregates raw signals from transaction logs, device telemetry, and third-party feeds.

- Feature Engineer Agent – Converts data into model-ready features.

- Model Scorer Agent – Runs real-time inference using fraud models.

- Explainability Agent – Generates rationale and risk attribution for human analysts.

- Mitigation Orchestrator – Executes remediation (hold, flag, approve).

This system is powerful—but dangerous without guardrails. Agents can overstep, leak PII, or make unsanctioned decisions. That’s where Aegis governs the boundaries.

Why Agentic Systems Need Security Meshes

Failure Modes in Agentic Fraud Detection

Failure Mode | Impact | Root Cause |

Rule engines miss new fraud vectors | False negatives, losses | Static logic |

Aggressive thresholds flag good users | Poor UX, churn | Lack of contextual intelligence |

Agents overreach access scopes | Compliance violation | Weak identity isolation |

Fraud models behave opaquely | Regulator pushback | No explainability or audit trail |

As these agents operate autonomously, the “who” and “what” of each decision must be verifiable. The absence of runtime policy enforcement creates the risk of agent privilege escalation or silent data exfiltration.

Governance Gaps in Multi-Agent Architectures

Even when FinTechs use IAM systems or API gateways, those layers lack fine-grained visibility into per-agent intent and parameters. IAM knows who called the API—but not why or whether it was appropriate. Security meshes like Aegis Gateway bring this missing enforcement logic to life.

Introducing Aegis: The Policy and Observability Fabric for Agentic AI

Aegis acts as the runtime enforcement gateway for AI agents—functioning like an Istio mesh purpose-built for multi-agent systems. It sits transparently between orchestrators (e.g., LangGraph, AgentKit) and tools (e.g., payment APIs, KYC services), inspecting and enforcing every call in real time.

Core Capabilities

- Agent Identity and Policy Enforcement

Each agent gets a unique, signed identity token. Policies define what tools it can call, with parameter conditions (e.g., amount <= $5000). Violations trigger auto-blocks or human approval workflows. - Runtime Call Interception

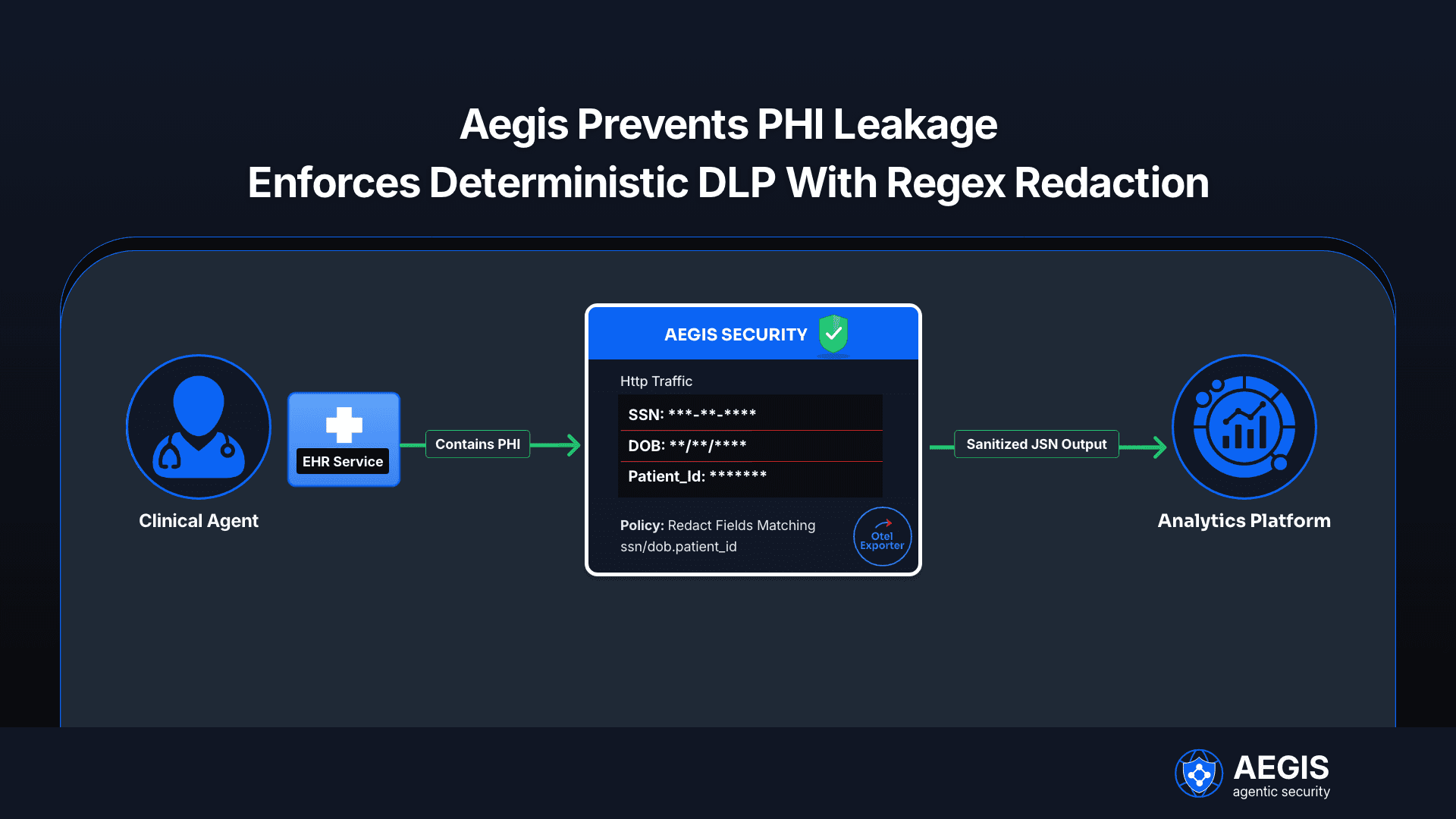

Aegis inspects each call’s context—agent ID, tool name, parameters, and parent-agent header—and decides allow, deny, sanitize, or approval_needed in under 20 ms. - Egress Control and PII Protection

Only approved endpoints (e.g., payment processors, internal APIs) are reachable. Any attempt to send data elsewhere triggers a deny decision and audit log. - Auditability and Explainability

Every action produces a signed OpenTelemetry span—capturing decision reason, policy version, and execution cost. Analysts can replay events for SAR/AML compliance.

Shadow Mode Deployment

Before enforcing, policies can run in “observe-only” mode to identify potential blocks without interrupting operations—ideal for FinTech pilots.

Applying Aegis to FinTech Fraud Scenarios

1. Payment Fraud Mitigation

In a payment flow, a detection agent flags a suspicious transaction (risk > 0.8). The investigation agent aggregates evidence and proposes a temporary hold. Before the hold exceeds 24 hours, Aegis enforces policy requiring human approval.

Outcome: Fraud blocked, customer notified, and audit logs automatically preserved.

Aegis Controls Applied:

- Parameter validation (max_hold = 24h)

- Per-agent confidence threshold

- Egress restriction on unverified account exports

- Audit trace with rationale and features attached

2. Account Takeover Defense

When the device agent detects login anomalies—like new devices and mismatched locations—it triggers a step-up MFA request. Aegis policies ensure these MFA challenges happen automatically while blocking further API access until validation.

Benefits: Real-time containment of ATO events without degrading the user experience.

3. Shadow Mode Pilot for FinTech Risk Teams

FinTech teams can begin by registering all AI agents in Aegis, mirroring production transactions for 30 days in shadow mode. Telemetry identifies potential violations and informs thresholds. After tuning, enforcement can be safely activated across payment corridors.

Comparative View: Legacy vs. Agentic Fraud Detection

Attribute | Legacy Rules Engine | ML Scoring Systems | Multi-Agent + Aegis Orchestration |

Latency | Batch (minutes–hours) | Seconds | Real-time (< 20 ms) |

Adaptability | Low (manual rules) | Medium (model updates) | High (dynamic multi-agent logic) |

Auditability | Minimal logs | Partial | Full, signed traces |

PII Protection | Manual | Limited | Policy-enforced DLP |

Human Oversight | Manual reviews | Partial | Automated escalation rules |

Compliance Readiness | Weak | Moderate | Strong (versioned, replayable) |

With Aegis, FinTech firms evolve from reactive fraud control to proactive, explainable, and enforceable AI risk governance.

Operationalizing Aegis in FinTech Environments

Step 1: Agent Registration and Policy Definition

Security teams define YAML policies per agent:

agent: finance-agent

allowed_tools:

- name: stripe-payments

actions:

- create_payment

conditions:

max_amount: 5000

approval_needed_above: 5000

Step 2: Enforcement in Runtime

When the finance agent calls the payment API, Aegis evaluates:

- Agent ID matches registry

- Amount ≤ 5000 → allowed

- Amount > 5000 → route to Slack/MS Teams for approval

- On approval → issue one-time override token

Step 3: Observability and Auditing

Aegis exports metrics on:

- Fraud cases blocked

- Time-to-decision

- Manual review volume

- False-positive/negative ratios

Security analysts can access these insights in Grafana dashboards or SIEM integrations.

Compliance, Governance, and Human Oversight

Regulatory frameworks such as PSD2, SOX, and AMLD6 demand attributable, explainable, and reversible decision flows. Aegis supports this through:

- Signed audit trails for every decision and override

- Versioned policy templates (e.g., max_hold, allowed_evidence_domains)

- Feature-level access controls for risk data

- Replayable traces suitable for regulator or SOC inspection

By embedding compliance into runtime architecture, FinTechs achieve continuous assurance instead of post-event remediation.

The Business Impact of Secure Multi-Agent Fraud Detection

Adopting Aegis for FinTech operations yields measurable benefits:

Metric | Before Aegis | After Aegis |

Mean Time to Detect Fraud | 12 min | < 1 s |

False Positive Rate | 3.8 % | 1.2 % |

Manual Review Volume | High | -65 % |

Compliance Audit Readiness | Reactive | Continuous |

Data Exfiltration Incidents | 2 per quarter | 0 |

These outcomes reflect a shift from manual oversight to policy-driven automation—enabling scalability without compromising control.

Best Practices for Implementation

- Start Small: Begin with high-value payment flows or corridors.

- Use Shadow Mode: Observe would-block events before enforcing.

- Define Metrics Early: Track FP/FN rate, manual-review volume, and latency.

- Integrate Human-in-Loop: Calibrate approval thresholds to avoid alert fatigue.

- Iterate Policies: Use telemetry to refine conditions and reduce false alerts.

Aegis’s architecture supports multi-tenancy, regional routing, and agent-level isolation, ensuring that even large MSSPs can manage FinTech clients securely and efficiently.

Future Outlook

By 2026, Gartner predicts that over 40% of financial institutions will use agentic AI for operational risk management. However, without robust governance, these systems could themselves become attack vectors. Aegis provides the enforcement plane that keeps this innovation aligned with compliance and trust.

Through its policy-as-code, runtime observability, and fine-grained control, Aegis transforms AI fraud detection from an experimental edge into a secure, auditable core capability of FinTech operations.

Frequently Asked Questions

1. How does Aegis differ from traditional fraud engines?

Aegis doesn’t detect fraud directly—it governs and secures the agents that do. It enforces real-time policies, validates parameters, and ensures every decision is explainable and auditable.

2. Can Aegis integrate with our existing fraud models?

Yes. Aegis runs as a proxy or middleware layer, integrating seamlessly with existing model scorers or orchestrators without code rewrites.

3. Does Aegis introduce latency?

Policy evaluations average under 20 ms, ensuring sub-second transaction decisions suitable for high-throughput payment environments.

4. How does Aegis help with compliance (e.g., AML, PSD2)?

Every decision, approval, and policy change is signed, versioned, and traceable—creating a continuous audit trail for regulators.

5. What’s the best way to pilot Aegis in FinTech?

Start with a 30-day shadow pilot for one payment corridor. Measure block decisions, adjust thresholds, and move to full enforcement after validation.

6. Does Aegis protect against prompt injection or data leakage in AI agents?

Yes. It enforces tool allowlists, redacts sensitive parameters, and blocks outbound traffic to unapproved domains, minimizing data exfiltration risks.